Paddy Carolan (QFA)

Paddy Carolan (QFA)

For years, tracker mortgages were seen as the gold standard – the deal you would never give up. But with European Central Bank (ECB) rates rising again and markets signalling more moves ahead, it is worth asking a question that would have sounded unthinkable a few years ago:

Is it time to let go of your tracker and lock into a competitive fixed rate instead?

This is especially important if you still have a meaningful balance and term left on your mortgage. The gap between where your tracker could go next and where 3–5 year fixed rates are today is no longer theoretical, it is visible in the data.

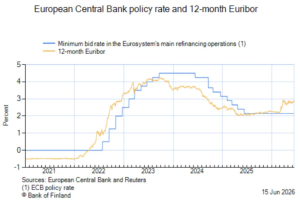

What the ECB vs Euribor graph is telling us

In the graph below, you can see two key lines:

- The blue line shows the ECB policy rate (the main refinancing rate).

- The orange line shows the 12‑month Euribor, which reflects what banks expect short‑term euro interest rates to be over the next year.

A few things stand out:

- When ECB rates started to rise sharply from 2022, 12‑month Euribor moved first and faster, anticipating those hikes.

- Even when the ECB paused or slowed increases, Euribor often stayed higher, reflecting market expectations of where rates might go next.

- Most recently, Euribor has kicked up again, even while the ECB rate has not yet moved by the same amount – signalling that markets see a real risk of further ECB hikes in the months ahead.

For anyone on a tracker mortgage, this matters because your rate is directly linked to the ECB. If the ECB moves up again, your tracker will go up automatically. Fixed rates, by contrast, are priced off longer‑term funding and bond markets, not the headline ECB rate alone.

Why trackers are not automatically “best” anymore

For a long time, the logic was simple:

ECB at or near zero + Tracker margin small = ultra‑low, hard‑to‑beat repayments

That world has changed. The ECB has already raised rates multiple times, and with inflation still above target and Euribor trending higher, there is a real possibility of further increases. In some scenarios, we could see a total rise of 0.5% or more over the next period, which would feed straight through to tracker customers.

Meanwhile, many lenders are still offering 3–5 year fixed rates in the region of 3%–3.5%, depending on loan‑to‑value, term and property type. In other words:

- Your tracker rate can keep climbing every time the ECB moves.

- A well‑chosen fixed rate can give you stability and visibility at a level that may already be cheaper – or soon become cheaper – than where your tracker is heading.

If you still see your tracker as something you can never give up, it is worth checking whether that belief is still based on today’s numbers, or yesterday’s assumptions.

What this could mean in practice

Let’s take a simple example to illustrate the point.

Assume:

- Outstanding mortgage: €150,000

- Remaining term: 20 years

- Current tracker margin: ECB + 1.25%

If the ECB rate moves up by a further 0.5% in total over time, your tracker rate would increase by the same amount. On a balance of €150,000 over 20 years, that kind of rise can add tens of euro per month to your repayments purely because the ECB has moved.

Now compare that with:

- A 3–5 year fixed rate in the 3%–3.5% range,

- Plus potential incentives such as 2% cashback on drawdown or monthly cashback on repayments from some lenders.

In many cases:

- The headline rate on the fixed option is already competitive versus your current tracker rate.

- The risk of further ECB hikes falls on the bank during the fixed term, not on you.

- The cashback can help cover legal and valuation costs and still leave you ahead.

Of course, the exact numbers depend on your balance, term, current margin and the specific fixed rates you qualify for – but the days of “tracker always wins” are gone for a lot of borrowers.

Who should be thinking about switching?

Switching off a tracker will not make sense for everyone.

If:

- Your remaining balance is small, and/or

- Your remaining term is short (for example, only a few years left),

the benefit of switching may be limited. In those cases, the simplicity of staying where you are may outweigh any modest saving.

However, if you still owe €150,000 or more, and have a decent term remaining (say 10–20 years), it is well worth exploring what is available on the market today.

For many people in this position, switching to a new lender offering acompetitive 3–5 year fixed rate, and a 2% cashback lump sum and in some cases a monthly repayment refund, can deliver both rate certainty and real savings, especially if ECB increases continue.

The key is to run the numbers based on your actual situation, not on rules of thumb.

What should you do next?

If you are still on a tracker, ask yourself:

- Do I know my exact current rate (ECB + margin)?

- Do I know what I would pay if the ECB rate rose another 0.5%?

- Have I compared that with available fixed rates on the market today?

- How much do I still owe, and how many years are left?

If the honest answer to most of these is “I am not sure”, it is time to get clarity.

At Irish Mortgage Corporation, we can:

- Review your current tracker in detail, including margin, balance and term.

- Compare it with the best fixed options available across multiple lenders.

- Factor in cashback and switching costs (legal and valuation) so you see the true net impact.

- Help you decide whether staying put, partially fixing, or fully switching is the right call for you.

You do not have to be a slave to your tracker rate.

If you still owe a meaningful amount, there may be a smarter, more stable option available – but the only way to know for sure is to look at the figures.

Contact me on

Tel: 01 669 1046

Email: paddyc@irishmortgage.ie

Here are some other related articles you might find helpful

Irish Mortgage Corporation comments on ECB rate rise